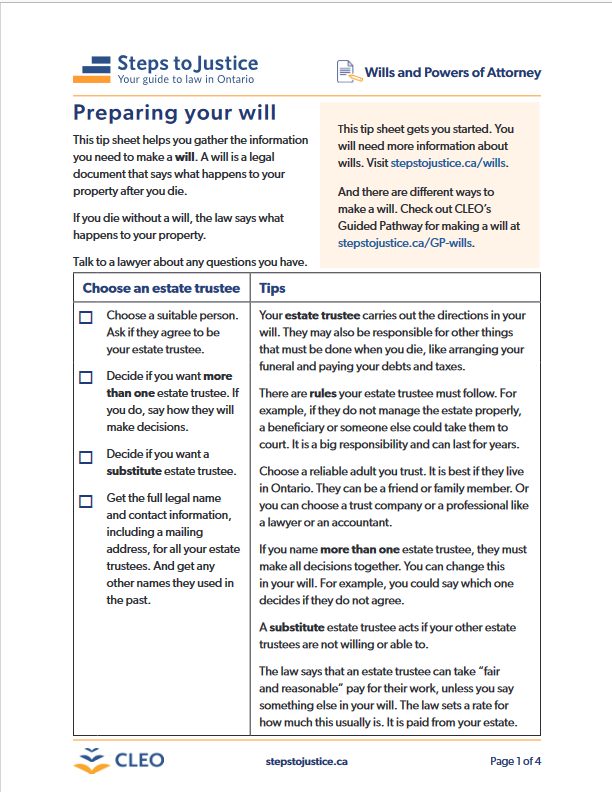

What do I need to think about when making a will?

Once you decide to make a will, think about:

- who to make your

- who your will be

- who will care for your minor children

- who will manage the property you left for your minor children

- who you want to give specific property to, like jewellery or a car

- what you want to happen at your funeral

If you have a or partner, you must each make your own will. You cannot make one will for both of you.

No one can force you to make a will, but it's usually a good idea to make one.

Who can make a will

To make a will you must be . This means that you understand:

- why you're making a will and the impact it will have

- how much property you have

- which dependants should be beneficiaries and the claims they might have if you do not leave them property in your will

Your will may be challenged if you make it when you're not mentally capable or if you do not include dependants.

A is a person you were supporting financially before you died or a person the law says you must support.

You must also be at least 18 years old to make a will. But you can be younger than 18, if you're:

- legally married,

- a member of the Canadian armed forces, or

- a sailor.

Get legal help

It's possible to make a will yourself. But it's usually a good idea to talk to an estates lawyer before making one. A lawyer can make sure you follow all the rules for making a will and help you make an that meets your needs.

For example, a lawyer can tell you how to reduce fees, advise you on the dependants you should include in your will, and explain what happens if a beneficiary dies before you do.

If you have a large or complicated , it might be a good idea to talk to a financial advisor and an estates lawyer.

If you have a simple estate, there are services such as Axess Law, that offer legal services at lower rates.

If your income is low, you can also call your local community legal clinic to see if they help with wills.

These places offer specific communities help with making a will:

- Queen’s University Elder Law Clinic helps older adults with low incomes who live in Kingston and in surrounding communities.

- The 519 Legal Clinic helps 2SLGBTQ+ people.

- Advocacy North for Elders and Seniors may help elders or older adults with low incomes living in Northern Ontario.

Estate plan

Making a will is only one part of an estate plan. Estate planning also includes things like:

- Reducing probate fees, for example, by making beneficiary designations and holding property jointly.

- Having a power of attorney for property so that someone can make decisions about your property if you become .

- Having a power of attorney for personal care so that someone can make personal care decisions if you become mentally incapable.

- Creating trusts to put conditions on how and when certain are distributed when you die.